The classic trope of broke millennials— It’s true for a reason.

“Millennials buying their first home today will pay 39% more than baby boomers who bought their first home in the 1980s.”

Millennials are tired of throwing their hard earned low wages at soaring rent prices in over-crowded urban cities. Owning a home or condo seems like a dream for those of us who won’t have their parents or guardians help with a down payment or mortgage bills.

Owning a home is possible, even for us millennials or gen Z. Below are some tips to help your dream become a reality!

1. What can I afford? (I can’t do a 20% down payment on a home!?)

The foundational question that can stop the average American in our tracks— what can you afford?

There is an answer: the question of affordability is paired with the loan you decide to go with.

I repeatedly came across information from family and friends that frightened me— that you had to have 20% down on a home. I thought to myself: a home that is $173,900 means that you need $34,780 for a down payment! I don’t have that kind of time to save up?!

Luckily, a 20% down payment on a house is not the only option. There are a few types of loans: conventional loans, rural loans, first time home owner loans, and etc. For example, with a conventional loan and depending on your credit score, a possibility 3% of the home price would be the down payment for a conventional loan. So, for a home that is $173,900 in an accepted offer… your down payment is around $5,217.00. That number is more achievable.

Below are some types of loans you may want to look into!

Conventional Loans

Conventional loans are originated and serviced by private mortgage lenders like banks, credit unions and other financial institutions, many of which also offer government-insured mortgage loans. In general, conventional loans don’t have some of the same perks as government-insured loans, such as low credit score requirements and no down payment or mortgage insurance.

It’s possible to get approved for a conforming conventional loan with a credit score as low as 620, although some lenders may look for a score of 660 or better. Even if you can qualify for a conventional loan, though, your interest rate will largely depend on your credit score and overall credit history. The better your credit is, the less you’ll pay in interest over the life of the loan.

https://www.experian.com/blogs/ask-experian/what-is-a-conventional-loan/

FHA Loans

Insured by the Federal Housing Administration, FHA loans typically come with smaller down payments and lower credit score requirements than most conventional loans. First-time homebuyers can buy a home with a minimum credit score of 580 and as little as 3.5 percent down or a credit score of 500 to 579 with at least 10 percent down.

https://www.bankrate.com/mortgages/first-time-homebuyer-loans-and-programs/

USDA Rural Loans

USDA loans are zero-down-payment mortgages for rural and suburban homebuyers. They’re mainly for borrowers who aren’t wealthy and can’t get a traditional mortgage. … A USDA home loan is a zero down payment mortgage for eligible rural and suburban homebuyers.

https://www.nerdwallet.com/article/mortgages/usda-loan

Military or Veteran Loans

If you are a veteran or military, often there are homeowner loans with a 0% down payment.

https://militarybenefits.info/va-home-loans-for-first-time-buyers/

2. Don’t forget to include mortgage insurance when calculating approximate costs.

There is only one down-side to a loan that does not have a 20% down payment: the mortgage insurance.

When you buy a home and don’t have at least 20 percent saved for a down payment, mortgage lenders want to protect themselves from risk if you can’t repay the loan. That’s why they require borrowers to pay for mortgage insurance, which protects the lender from loss when a borrower can’t repay the loan.

With a conventional loan, private mortgage insurance, or PMI, of up to 1 percent or more of the loan amount is charged every year until you have at least 20 percent equity in your property…

https://www.bankrate.com/mortgages/fha-mortgage-insurance-guide/

A typical loan will have the mortgage, the taxes, and the house insurance included in the bill for the first year. Mortgage insurance is where the loan company is safe-guarding their investment of offering you a loan and charging you insurance on the loan itself. Most of the time, this insurance is worth owning your home. You can calculate your mortgage insurance here.

3. Your credit score, unfortunately, does matter.

A higher credit score can really help you find a lower interest rate for your home and have the mortgage company want to accept your loan application. A lower interest rate means more money in your pocket that the bank can’t have.

You can get your free credit score through Credit Karma. With Credit Karma, your credit score will not be affected by checking your credit. A recommended score is definitely about 650. The higher, the better.

Your bank is a great start when looking into applying for a home loan. If they’re asking for more than 3.5% interest, I would start looking at other companies to apply to.

“But won’t my score be affected with each time a company runs my credit?”

When you apply for a loan and the lender runs your credit check, your score will be slightly penalized for just checking your credit score. However, you will have a set amount of time after that initial first credit score pull to shop around and not be further penalized.

Some realtors will require a pre-approved amount from a mortgage company prior to even showing you houses. Make sure you have your finances figured out and a pre-approved amount prior to being shown homes.

For example, I used Movement Mortgage for my loan. https://movement.com/

Also, here is a list of popular mortgage lenders.

4. Weigh in on your needs vs. wants and have a clear picture of your ideal home.

What are your must-haves? What are your “I can live without this,” bucket list items?

Write down the top 5 things you will not flex on in a future home. (Don’t worry, these things can change as you find out what is more important to your needs.)

For example, here were some of mine when house hunting:

Needs

- I need the home within a 30 minute commute of my current job or future job opportunities (city).

- I need 2 bathrooms so my future guests or child can have a spare bathroom.

- I need a basement for extra storage and easy access to the underside of my house.

- I need to not be near any major water source to reduce the likelihood of flooding.

- I need a lot of light in my space.

Wants

- I would like a large bathtub in the bathroom.

- I would like a finished basement.

- I would like a heat pump instead of a furnace.

- I would like a large yard for outdoor space.

The wants are things you can flex on, or that you can possibly create later with renovations.

As you tour homes with your real estate agent, you may find that there are things on your “need” list that become “wants.”

5. Take ownership of your future home by searching before your realtor does.

I’ve often found that my real estate agent couldn’t keep up with my own email account. I would send her homes I wanted to see before she could even set up a date to view older homes that had been on the market in the area.

For example, two houses we put offers on had an accepted offer within three days. The posting for the house would go up, we would view the house the next day (usually Friday) and then we would place an offer by Monday morning. The housing market is quick when the houses are fair prices in a good neighborhood. We would have never even had the chance to even see the home if I waited on my realtor for house showings.

I highly recommend Realtor.com for house hunt, unless you are paying with straight cash (then Zillow.com has more options like “for sale by owner” or foreclosures.) You can adjust your settings for price, location, bedrooms, bathrooms, and etc.

6. It is not uncommon to offer the asking price on a house.

(The “old timers” will choke when they hear this one) On one of the houses my family put in an offer for, we actually offered the asking price itself for a home— $155,000. Unbelievably, the seller rejected stating they had a higher offer of $5K more on the asking price.

Our family relatives told us repeatedly to “not offer at asking price,” yet, the market is divergent from when they bought a house back in the 80’s or 90’s. If you live in a highly competitive market, offering the asking price is not shameful– but recommended on hot ticket homes.

7. Writing a letter with your offer could weigh things in your favor.

This one tip helped me get an accepted offer on a house where another house hunter had placed a higher amount than me! Writing a letter with your offer is the most simple and best practice you can add. It tells the seller just who put in the offer and why you want to live in their cherished abode.

Click here for the PDF of the letter I wrote for our approved housing offer– it made a great impression!

Here are tips on how to write a great offer letter for a house.

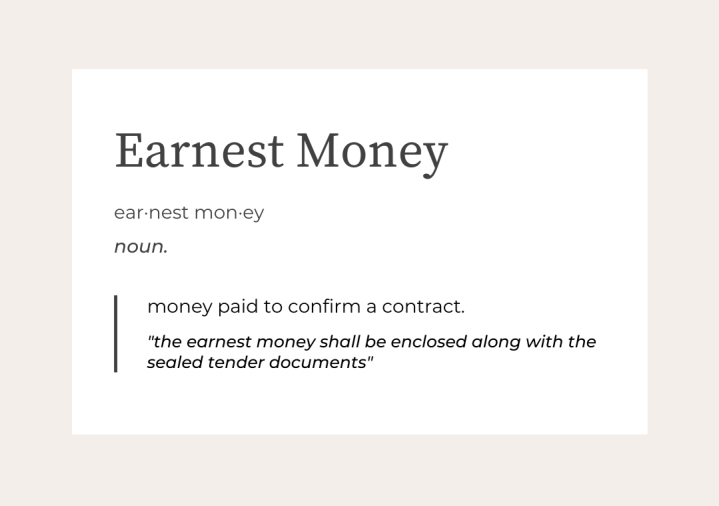

8. Save up extra $ for due diligence and earnest money.

You’re preapproved for a home loan amount, you’ve found your perfect home, and now you’re going to place an offer. Great! Here are the terms you to need to know:

Due Diligence – Money you will not receive back, if your offer is accepted. It’s a smaller amount usually around $200-$300 that sets in motion that as a buyer you will do your “due diligence” with inspections and learning more about the property. Even if you were to discover something awful, like mold in the house, you will not be able to receive this money back.

Earnest money – Also known as “honest money.” This money you could receive back if you pulled your accepted offer during your due diligence period. This money usually goes in an account with the closing attorney and will only be given to the seller’s after the closing agreements are signed. This is usually around $1000 for an average home.

9. Inspections are worthless if you’re not there.

Your inspections are vital to a home’s wellbeing for the first time you really get to look into the maintenance of your building. A good inspection will handle everything from structural problems, to roof quality, to draftiness, and even to possibly electric problems. A good inspector will turn on everything in the house and see if everything is working properly.

It is vital that at least one of you who is purchasing the home interacts with your inspector. You’ll learn vital information about your house— where the water turn off is, where the oil filter is for a furnace, or if there is mold under the sink. Do your research and expect to pay $350.00 for a basic inspection, and an additional $350.00 for anymore specific inspections. For example, you may want to have a radon inspection for your basement or a septic tank inspection if you don’t have sewer access on your future home.

10. Arming yourself with knowledge is priceless.

Before you place money on one of the biggest investments in your life, I highly suggest that you read up on how the process works.

The book that prepared me the best for the entire process is this book:

The Essential First-Time Home Buyer’s Book: How to Buy a House, Get a Mortgage, And Close a Real Estate Deal by Editors at Realtor.com https://www.amazon.com/Essential-First-Time-Home-Buyers-Book/dp/1543965717

It helps explain each process of the home buying from beginning to end, and even what to do after you land a home.

This is a very well-written article, and I feel will be very helpful to those of us our age in need of advice in buying a home for the first time. It’s a very stressful process, and you simplified it that’s easy to understand.

LikeLike